2026 Guide: Top Tips for First-Time Home Buyers

First time home buyer tips are your lifeline when you are excited about your first home and a bit overwhelmed by the home buying process. Buying a home is probably the largest financial decision you will make. It feels big for a reason. With the right preparation and clear steps, the path can be smooth and honestly pretty rewarding.

You will get practical advice you can use right away, not fluff. We will cover financial preparation, understanding mortgages and preapproval, finding the right home, navigating closing costs and paperwork, and settling into homeownership without second-guessing every box you unpack. That means credit scores and down payments, the main loan types, how to compare lenders, writing a strong offer, what inspections and appraisals actually do, and the first things to handle after you get the keys. These first time home buyer tips are especially useful in competitive markets like Houston and surrounding Texas communities where homes can move fast and details matter.

My goal is to help you feel confident, not rushed. Expect plain language, real checkpoints, and a few smart moves to save time and stress (and a couple of myths to ignore). And we will take it step by step so nothing slips through the cracks. First up: getting your finances ready.

Preparing Your Finances: Building a Strong Foundation

Financial prep is the first real milestone in the home buying process. Before you browse listings or schedule showings, you want your money picture tight. That means understanding your credit, setting a realistic home buying budget, and having cash reserves ready. Lenders look at these details during mortgage preapproval, and that early check can make or break your momentum. Get this foundation right and the rest of the process gets a lot easier.

Understanding Your Credit Score and How to Improve It

Your credit score does two big things. It helps determine if you qualify and it influences your interest rate and monthly payment. Credit score requirements vary by loan type. For a conventional loan620. For an FHA loan580 for 3.5% down, and some may be eligible between 500-579 with a larger 10% down payment. VA loans do not have a government-set minimum score, but many lenders use guidelines around 620. USDA loans also do not have a hard minimum set by the agency, though many lenders prefer 640 for streamlined automated approval and may consider lower with additional documentation. Higher scores usually mean better pricing and lower mortgage insurance costs. Start by checking your credit reports for accuracy at AnnualCreditReport.com and review guidance from the CFPB on disputes here: CFPB credit report disputes.

- Pay every bill on time. Payment history is the biggest slice of most credit scoring models.

- Reduce credit card balances. Aim to keep utilization below 30% of your limit. Lower is better.

- Avoid new credit applications for a few months before mortgage preapproval. Hard inquiries can nudge scores down.

- Dispute any errors on your credit reports using the bureaus’ online portals. Keep documentation of outcomes.

- Keep old accounts open and active. Longer credit history typically helps.

Even small score bumps can save you real money over a 30-year loan. So this part is worth the focus.

Saving for Your Down Payment: How Much Do You Really Need?

You do not need 20% down to buy your first home. Many first-time buyers qualify for as little as 3% down on certain conventional programs, and FHA allows 3.5% down for buyers who meet credit and income guidelines. A bigger down payment can lower your monthly cost and may eliminate private mortgage insurance on conventional loans. But starting with 3% or 3.5% is common and perfectly fine if it keeps your overall finances strong. Just remember to plan for closing costs too, which are typically separate from your down payment.

Texas buyers have access to several reputable down payment assistance options. The Texas Department of Housing and Community Affairs (TDHCA) and the Texas State Affordable Housing Corporation (TSAHC) both offer programs that may provide grants or repayable second liens to help with down payment and closing costs, typically with income, credit, and homebuyer education requirements. In Houston, the City of Houston Housing and Community Development office publishes current assistance programs and eligibility details. Availability changes, so always check current guidelines and talk with a lender that regularly works with Texas assistance programs.

Some buyers in the Houston area work with real estate professionals like Allen Markel who offer programs such as Buy Before You Sell, which allows you to secure your next home before selling your current one, reducing financial pressure.

If you are starting from scratch, automate savings on payday, stash windfalls like tax refunds, and keep your down payment in a high-yield savings account so it is safe and accessible when you are ready to buy.

Building an Emergency Fund Beyond Your Down Payment

Your down payment is step one. Your emergency fund is step two. Aim for 3-6 months of essential living expenses set aside, separate from the down payment money. This cushion covers surprises like a leaking water heater, a sudden car repair, or a gap in income. Homeownership adds extra variables. Think HVAC repairs during a Texas summer, a roof patch after a windstorm, a plumbing leak behind a wall, or an escrow shortage when property taxes adjust. Those hits are rarely convenient. Having cash saved keeps those moments from turning into debt.

Quick way to size your fund: total your non-negotiable monthly costs – housing, food, insurance, transportation, childcare, minimum debt payments – then multiply by 3-6. If you spend $4,000 a month, a target range is $12,000 to $24,000. If that number feels large, build it in stages. First one month, then three, then six.

This is separate from your down payment so you do not drain your safety net on closing day. Lenders do not require an emergency fund for every loan type, but you will sleep better once you have it.

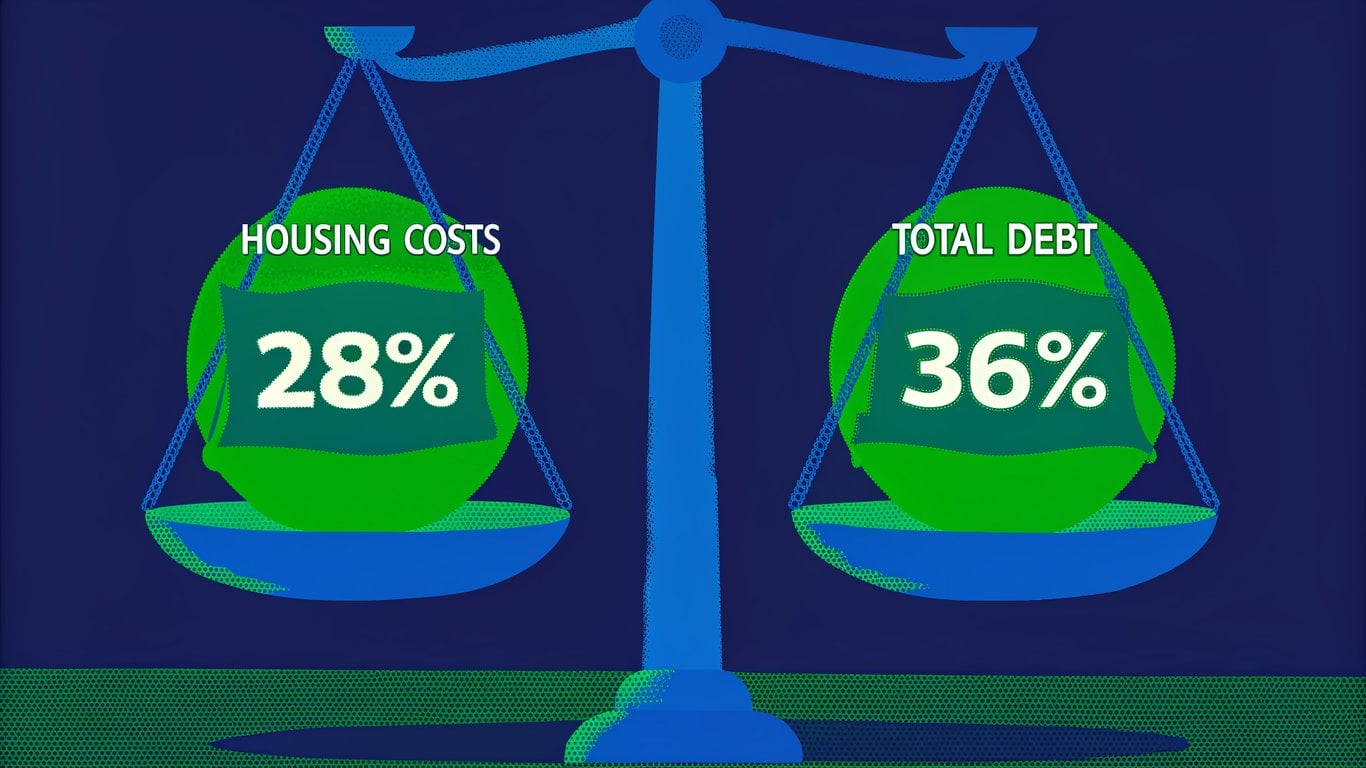

Calculating Your True Home Buying Budget

A time-tested guideline is the 28/36 rule. Keep your housing costs – principal, interest, property taxes, homeowners insurance, and HOA dues – at or below 28% of your gross monthly income. Keep your total monthly debt payments – housing plus all other debts – at or below 36%. It is a guide, not a law, but it is close to how many lenders think when they review your mortgage preapproval.

Example: if your household earns $90,000 a year, that is $7,500 a month before taxes. 28% of $7,500 is $2,100. That is your target max for the full housing payment. 36% of $7,500 is $2,700 for all debt combined. If you already pay $400 for a car and $200 for student loans, you have $600 in non-housing debt. $2,700 – $600 = $2,100 available for housing. That lines up with the 28% cap. From there, a lender can translate that payment into a price range based on current interest rates and taxes.

When you build your home buying budget, factor in more than the mortgage:

- Property taxes – Texas rates vary by county and school district. They can be a substantial part of your payment.

- Homeowners insurance – lenders require it, and costs can vary based on location and coverage.

- HOA or condo fees – common in master-planned communities and condos.

- Utilities – electricity, gas, water, trash. Older or larger homes often cost more to run.

- Maintenance and repairs – many owners set aside 1-2% of home value annually.

These numbers help you shop confidently. They also prepare you for a smoother mortgage preapproval, since lenders will evaluate the same inputs when verifying your price range.

Getting Your Debt-to-Income Ratio in Order

Your debt-to-income ratio (DTI) compares your monthly debt payments to your gross monthly income. Lenders care because it measures repayment capacity. Many aim for a maximum of 43% for total DTI. Some programs may allow higher with strong compensating factors, but keeping DTI lower generally improves approval odds and terms. To calculate yours, add up your monthly debt payments – including the projected mortgage payment – then divide by your gross monthly income.

- Pay down revolving balances first. Reducing credit card payments can drop DTI quickly and help credit scores too.

- Avoid taking on new loans or financing big purchases until after closing.

- Consider refinancing or consolidating higher-rate debts into a lower monthly payment if it reduces total cost over time. Weigh fees carefully.

- Boost income and document it. Overtime, bonuses, or a second job can count if it is consistent and verifiable. If in doubt, ask your lender what will qualify.

- If you need guidance, a HUD-approved housing counselor can help you map a plan: Find a HUD-approved counselor.

Tightening up DTI before you apply can be the difference between a prequalification and a rock-solid preapproval. Pair that with the 28/36 rule, a realistic home buying budget, and a healthy emergency fund, and you will be in a strong position to buy with confidence.

Navigating Mortgages and Preapproval

Mortgages are the vehicle that makes homeownership possible for most first-time buyers. You borrow a large chunk of the purchase price and pay it back slowly, with interest. That means the loan you choose, the mortgage lender you pick, and getting strong mortgage preapproval all matter more than most people expect. A few smart moves here can save real money and reduce stress when you find the right place.

Understanding Different Types of Home Loans

Loan Type | Minimum Down Payment | Credit Score Requirement | Best For |

|---|---|---|---|

Conventional | As low as 3% (for eligible first-time buyers) | Typically 620+ | Borrowers with solid credit and steady income who want PMI that can be removed later |

FHA | 3.5% with 580+; 10% with 500-579 | 580 for 3.5% down; 500 minimum with larger down | Buyers with lower credit scores or higher DTI who need more flexible guidelines |

VA | 0% (for eligible service members, veterans, and some surviving spouses) | No VA minimum; many lenders look for 620+ | Eligible borrowers seeking competitive rates and no down payment |

USDA | 0% (property and income eligibility required) | Typically 640 for streamlined approval | Low-to-moderate income buyers in eligible rural or suburban areas |

A conventional loan is the most common option. Private mortgage insurance (PMI) applies when you put less than 20% down, but you can usually remove it once you reach about 20% equity. That flexibility is a big draw for many buyers. FHA loans, backed by the Federal Housing Administration, make qualifying easier if your credit is still a work in progress. They come with an upfront and annual mortgage insurance premium. In many cases it lasts for the life of the loan unless you make a larger down payment. You can learn more at HUD.gov.

VA loans are a standout benefit for qualifying service members, veterans, and surviving spouses. There is no down payment requirement and no monthly mortgage insurance. There is typically a one-time funding fee unless you qualify for an exemption. Details are at VA.gov. USDA loans offer no down payment in eligible areas, plus income limits to keep the program focused on need. There is a guarantee fee that functions somewhat like insurance. Check property eligibility and program basics at USDA Rural Development.

No single loan is best for everyone. If your credit is strong and you want the option to drop PMI later, a conventional loan probably fits. If you need more flexible credit or debt allowances, FHA can be a bridge into homeownership. If you served, VA is hard to beat. If your target area qualifies and your income fits, USDA can open doors with zero down. The right choice comes down to your credit, savings, income, and where you plan to buy.

Prequalification vs. Preapproval: Know the Difference

Prequalification is an informal estimate based on information you provide to a lender. It is quick and useful for early planning, but it is not verified. Preapproval is a conditional commitment from a lender after they check your credit and review your income, assets, and debts. You will get a preapproval letter that sellers can trust. In multiple-offer situations, preapproval gives you negotiating power and signals you are ready to close.

- W-2s for the last 1-2 years

- Recent pay stubs (typically 30 days)

- Recent bank statements (usually 2-3 months)

- Most recent federal tax returns

- Government-issued ID

Expect a hard credit check during mortgage preapproval and be ready to explain large deposits, job changes, or new credit lines. None of this is meant to trip you up. Lenders just need a clear picture so they can issue a strong, reliable letter.

Shopping for the Best Mortgage Lender

- Interest rates and whether points are required to get them

- Loan fees and lender credits offered

- Total closing costs and third-party fees

- Customer service and responsiveness

- Digital tools for uploading documents and tracking milestones

- Local market knowledge and reputation

Compare at least three lenders. Small rate or fee differences can add up to thousands over the life of a loan. After you apply, lenders are required to provide a Loan Estimate within three business days that outlines your rate, APR, payment, and closing costs. Lining up these documents side by side makes real comparison possible. The Consumer Financial Protection Bureau has a helpful explainer at consumerfinance.gov. Ask questions about rate locks, timing, and what could change before closing. It is your money, so it is worth being picky.

What to Expect During the Mortgage Application Process

- Application submission

- Documentation review

- Home appraisal

- Underwriting

- Conditional approval

- Final approval

- Closing

Application submission: you complete the application, consent to a credit check, and upload your documents. Documentation review: the loan team checks your income, assets, and debts to verify everything matches your application.

Home appraisal: an independent appraiser evaluates the property to make sure the value supports your loan amount. The home appraisal protects both you and the lender. If value comes in low, you may renegotiate, increase your down payment, or in some cases change loan options.

Underwriting: a professional risk review where the underwriter applies guidelines for your loan type. They confirm your finances and the property meet the program rules. This is where edge cases get sorted out.

Conditional approval: you are approved with a few conditions. Common ones include an updated pay stub, a letter of explanation for a credit item, clearer documentation for a large bank deposit, or finalizing homeowners insurance. Title work must also clear with no issues.

Final approval: often called clear-to-close. Your conditions are met, the appraisal is accepted, title is clear, and your closing figures are set. Closing: you review and sign your documents, pay your cash to close, and the loan funds. Your earnest money deposit is typically credited toward your down payment and closing costs at this stage.

Understanding Closing Costs and How to Prepare

Closing costs are the fees and prepaids to complete your home purchase and set up your loan. They typically total about 2% to 5% of the purchase price, on top of your down payment. You will also see owner’s and lender’s title insurance on your final figures, which protects against certain title defects. Lenders will give you a Loan Estimate early and a Closing Disclosure near the end, so you can see these numbers ahead of time and plan.

- Loan origination and underwriting fees

- Appraisal fees

- Title search and title insurance

- Attorney or settlement agent fees

- Prepaid property taxes and escrow setup

- Prepaid homeowners insurance

- Recording and transfer fees

You can sometimes negotiate seller concessions to help cover a portion of these costs. This works best when the market is less competitive or the seller wants a faster close. Each loan type limits how much a seller can contribute, and your lender can explain those caps. If a seller credit is not available, ask your lender about pricing a small lender credit into your rate to offset fees. There is no one right move. The goal is to structure the deal so your upfront cash, monthly payment, and time horizon all make sense together.

Finding and Securing Your First Home

You have your budget, your credit in shape, and your preapproval in hand. Now comes the fun part. It is time to turn your spreadsheets into doorways and neighborhoods. House hunting moves fast, and small decisions stack up quickly. A clear plan, plus the right people in your corner, helps you avoid shiny-object distractions and focus on a home that actually fits your life.

Choosing the Right Real Estate Agent

A great real estate agent is your strategist, deal-spotter, and guardrail. A dedicated buyer’s agent represents only you during the search and negotiations. They track new listings, analyze comps, pressure-test pricing, and guide you through contracts. Buyer representation is typically compensated through the transaction, so it usually does not add an out-of-pocket cost for first-time buyers. Models can vary by market and brokerage though, so ask how compensation works up front. Clarity prevents surprises.

- How much experience do you have in my target areas, and which neighborhoods do you know best?

- How many first-time buyers did you help in the last year, and what were the common roadblocks?

- What is your communication style and cadence? Text, calls, email, or your app of choice?

- What is your availability for weekday evening showings and weekend tours?

- Can you share 2 to 3 recent buyer references I can contact?

- How do you approach offer strategy in multiple-offer situations and in a buyer’s market?

- What local programs or incentives should I know about, including any down payment assistance or tax exemptions?

- Do you have a vetted network for lenders, inspectors, and contractors, and how do you handle potential conflicts of interest?

Local experience matters a lot in Greater Houston. Neighborhoods just a few exits apart can have very different property taxes, HOA fees, commute patterns, and flood histories. An agent who knows Katy vs. Cypress vs. Montgomery can flag things you might miss, like a master-planned community’s amenity costs, noise from a nearby freight line, or how traffic ebbs and flows along I-10, 290, or the Grand Parkway. That level of context helps you pay the right price for the right house.

Defining Your Home Must-Haves vs. Nice-to-Haves

Before you step into your first showing, define a short list of non-negotiables. The must-haves vs. nice-to-haves framework keeps you from falling for a pretty backsplash that blows your budget or ignoring a deal-breaker like a punishing commute. Keep it tight. Four to six must-haves is plenty. Everything else goes in the nice-to-have column so you can stay flexible when a strong listing hits the market.

Must-Haves | Nice-to-Haves |

|---|---|

Number of bedrooms that truly fits your household | Updated kitchen with modern finishes |

Location that aligns with your daily commute or transit options | Pool or spa for recreation |

Total monthly budget that stays within your comfort zone | Large yard or extended patio |

Preferred school district or feeder pattern | Dedicated home office or flex room |

Be honest with yourself and your agent. If you must live within 20 minutes of work, say so. If your budget is the line in the sand, protect it. Then allow smart tradeoffs when the right house shows up. You might not get the pool now. You can add an office later. Staying flexible while honoring your core priorities is how first-time buyers win.

Researching Neighborhoods and Communities

- School ratings and feeder patterns, even if you do not have kids. They affect resale interest.

- Crime statistics and recent trends using official local data sources.

- Property tax rates and any special assessments that impact your monthly payment.

- Commute times at rush hour, not just at noon on a Saturday.

- Nearby amenities like parks, grocery stores, healthcare, and trails.

- Future development plans that could add value or introduce noise and traffic.

- HOA fees, rules, and amenities in master-planned communities.

Visit neighborhoods at different times of day. Morning school drop-off tells you a lot. So does a 6 p.m. drive when everyone is heading home. Pay attention to street lighting, parking, and noise. In Texas, budget time to understand local taxes and assessments. The Texas Comptroller explains how property tax works, and county appraisal districts publish rates and exemptions. Master-planned communities often have higher HOA fees to maintain pools, trails, and security. Ask about any municipal utility district or public improvement district assessments as well. If flood risk is a concern for you, review FEMA maps at the Flood Map Service Center and ask your insurance agent what a policy might cost.

Making a Competitive Offer in Today’s Market

A strong offer is more than a number. It is a complete package that makes the seller feel confident about closing. Core components include your proposed purchase price, the earnest money deposit that shows you are serious, any contingencies such as financing, appraisal, or inspection, and your preferred closing timeline. Your lender letter matters too. A fully preapproved buyer often looks safer than a buyer who is only prequalified.

Strategy shifts with market conditions. In a hot area or price point with multiple bids, the cleanest offer frequently wins. That might mean tightening contingency windows, being flexible on the seller’s preferred closing date, or offering rent-back terms if needed and allowed. In a true buyer’s market with more inventory and slower sales, you can usually negotiate more on price, repair credits, or concessions. Your agent should tailor the plan to the specific house and the seller’s priorities.

An escalation clause can help when you expect multiple offers. It says you will beat a competing offer up to a stated cap, usually with proof of that competing offer. This tool keeps you in the game without wildly overbidding at the start. It is not always the right move. If the home later fails to appraise at the escalated price, you could face a funding gap. Discuss guardrails with your agent and lender before you use one, including whether you are comfortable bringing extra cash or adjusting terms if the home appraisal comes in low.

The Importance of Home Inspections and Appraisals

A home inspection and a home appraisal are not the same thing. An inspection is a detailed review of the property’s condition for your benefit. It helps you understand repair needs and future maintenance. An appraisal is an independent opinion of value ordered by your lender. It protects you and the lender from overpaying relative to recent comparable sales.

- Foundation and signs of movement or moisture

- Roof condition, flashing, and estimated remaining life

- HVAC systems and basic performance

- Plumbing, water heater age, and visible leaks

- Electrical panels, outlets, and safety issues

- Structural elements and visible framing concerns

A strong inspection report gives you options. With an inspection contingency, you can request repairs, ask for a closing credit, or walk away if the findings are serious and you are within your option period. Your agent will help you focus on items that matter to safety, structure, and systems. Cosmetic nitpicks rarely move the needle with sellers. If you are new to inspections, the American Society of Home Inspectors has a helpful primer on what to expect: What Is a Home Inspection?. Many inspectors also follow standards of practice like those published by InterNACHI.

Appraisals are about value, not condition. The appraiser checks recent comparable sales and the home itself to form an opinion of market value. If the appraisal is at or above your contract price, you are good to go. If it is below, you and the seller need a plan. Options typically include negotiating a lower price, meeting in the middle, or bringing additional cash to cover the gap if your lender will not finance above the appraised value. In some cases your lender can submit a reconsideration of value with stronger comps. Your agent and lender will guide the next move so the deal still makes sense.

Bottom line. Treat inspections and appraisals as decision tools. They are there to protect you, not slow you down. Listen to the professionals, ask every question you have, and use the findings to fine-tune your offer, your budget, or in rare cases your exit plan.

Closing and Moving Into Your New Home

You did the tough stuff. You saved, shopped, and negotiated. Now you are almost at the finish line, and it feels pretty great. The last stretch is mostly logistics and careful review. A little preparation now will help you close with confidence and start life in your new place on the right foot.

Understanding the Closing Process and Timeline

Once your offer is accepted, closing typically takes 30-45 days. That window gives your lender, the title company, and everyone else time to tie up loose ends. In Texas, closings are commonly handled at a title company. Your job is to track key milestones, respond quickly to requests, and review every document that hits your inbox.

- Final loan approval

- Title search completion

- Final walk-through

- Closing Disclosure review – 3 days before closing

- Closing day

- Key handover

Final loan approval: After you go under contract, underwriting verifies your income, assets, credit, and the property details. Avoid new debt, stay employed, and keep funds stable. If anything changes, tell your lender right away. Surprises can delay or derail approval.

Title search completion: The title company checks public records for liens, easements, and ownership issues. You will see title documents and options for title insurance. A lender policy is typically required. An owner’s policy is optional but common because it protects you from covered title defects. Learn more from ALTA’s consumer guide: What Is Title Insurance.

Final walk-through: You will confirm the home’s condition matches the contract and any agreed repairs are done. It is not a new inspection. It is a quick but important check to make sure nothing changed after your offer.

Closing Disclosure review: Your lender must provide the Closing Disclosure at least three business days before closing. Compare it line by line to your original Loan Estimate. Look at the interest rate, loan amount, monthly payment, and all closing costs. The CFPB has a helpful guide: What is a Closing Disclosure? and What is a Loan Estimate?.

Closing day: You will sign the final loan and title documents, pay your closing costs and prepaid items, and bring required identification. The title company coordinates with your lender and the seller to fund once everything is signed.

Key handover: After the loan funds and the deed records with the county, you get your keys. That is the best email you will get all year.

Final Walk-Through: What to Check

The final walk-through usually happens 24-48 hours before closing. Plan 20 to 45 minutes. Bring your contract and inspection report. Take photos and video as you go. If the home is occupied, be respectful but thorough.

- Verify all agreed-upon repairs are completed and documented

- Confirm appliances and fixtures are present and working as expected

- Check for new damage since inspection – walls, floors, windows

- Run water at sinks, showers, and flush toilets to confirm plumbing

- Test lights, outlets, HVAC, and that utilities are functioning

- Confirm garage door openers, keys, mailbox keys, and remotes are available

Find a problem? Do not ignore it. Ask your agent to document the issue and propose a solution before closing. That could be a repair completed prior to signing, a seller credit, a small escrow holdback until work is done, or a brief delay. Lender and title company rules vary, so your options depend on what they allow. The goal is to protect you without jeopardizing funding.

Closing Day: What to Expect and Bring

Plan for a 1- to 2-hour appointment at the title company or an attorney’s office, depending on your state. You will review every page, sign a stack of documents, and wire or deliver funds for closing costs and prepaid items like homeowners insurance and property taxes. If you are wiring funds, verify instructions by phone using a known number. Wire fraud is a real risk. The CFPB explains how to protect yourself: Avoid Wire Fraud at Closing.

- Government-issued ID (driver’s license or passport)

- Cashier’s check or proof of wire transfer for closing funds

- Proof of homeowners insurance with effective date on or before closing

- Any documents your lender or title company requested in advance

Documents you will sign include the promissory note that sets your repayment terms, the deed of trust or mortgage that secures the loan, the final Closing Disclosure, and title documents. If you opted for an owner’s title insurance policy, you will acknowledge that too. Ask questions any time. Good pros want you to understand what you are signing. When everyone signs and the lender releases funds, the title company records the deed. Then it is key time.

Moving In: First Steps in Your New Home

- Change the locks and reprogram smart locks and garage keypads

- Locate the main water shut-off valve and electrical panel and label breakers

- Set up utilities and internet in your name, and snap meter photos on day one

- Update your address with USPS: Official USPS Change of Address

- Test smoke and carbon monoxide detectors and replace batteries

- Create a home maintenance schedule for filters, gutters, HVAC service, and seasonal checks

Plan for ongoing home maintenance. A simple rule of thumb is to set aside 1-2% of your home value per year for repairs and upkeep. Some years you will spend less. Some years a water heater or roof eats the budget. Also track property taxes and homeowners insurance renewals. Many loans collect these in escrow, but you are still responsible for changes. If you are buying your first home but still own another property, programs like Allen Markel’s Sell and Stay option allow you to sell your current home while continuing to live in it during your transition, providing financial flexibility without the stress of rushed moving timelines.

Building Equity and Planning for the Future

Home equity is the difference between what your home is worth and what you owe on your mortgage. You build equity two ways. Each monthly payment reduces your principal a little. Over time, your home may also appreciate. Markets move in cycles, so focus on steady progress. The longer you own, the more equity typically compounds.

- Make extra principal payments when possible. Even small amounts help over time.

- Invest in smart improvements that tend to add value, like energy-efficient upgrades or well-done kitchens and baths.

- Maintain the property well. Preventive care often costs less than major repairs and helps preserve value.

Think long term. Your first home is a foundation for wealth, not the final destination. Maybe you will refinance later, or maybe you will leverage equity for a future move. For now, set a plan, budget for maintenance, and enjoy what you just accomplished. You did something big. And it is just the start.