If you’re self-employed and trying to buy a home in Texas, you’ve probably heard about stated income loans. Maybe a friend mentioned them, or you saw an ad promising “no tax returns required.” Here’s what you need to know right away: true stated income loans don’t exist anymore. They haven’t since 2008.

But that doesn’t mean you’re out of options. Modern alternatives serve the same purpose, just with different names and slightly more documentation. These programs recognize that your tax returns don’t tell the whole story of your financial success.

The Original Stated Income Loan: What It Was and Why It No Longer Exists

Before 2008, you could literally state your income on a mortgage application without proving it. Lenders took your word for it. No pay stubs, no tax returns, no bank statements. Just your signature saying “I make $X per year.”

These loans earned nicknames like “liar loans” and “no-doc loans.” They weren’t all fraudulent, though. Many self-employed borrowers used them legitimately because their tax returns showed minimal income after business deductions.

The 2008 financial crisis changed everything. Regulators determined that stated income loans contributed to the housing collapse. The Dodd-Frank Act and new ability-to-repay rules essentially eliminated them. Lenders now must verify that borrowers can actually afford their mortgages.

Modern ‘Stated Income’ Alternatives: What Lenders Actually Offer Today

When lenders advertise “stated income loans” today, they’re using outdated terminology. What they’re really offering are alternative documentation loans. You still need to prove your income, just not through traditional W-2s or tax returns.

These modern programs fall under the non-QM (non-qualified mortgage) category. They don’t meet standard Fannie Mae or Freddie Mac guidelines, but they’re perfectly legitimate and regulated. Lenders verify your ability to repay through bank statements, asset accounts, or rental income instead of traditional employment documentation.

Who Qualifies as Self-Employed in Texas Mortgage Lending

For mortgage purposes, you’re considered self-employed if you own 25% or more of a business. This includes sole proprietors, independent contractors, freelancers, and gig workers. If you’re a 1099 contractor rather than a W-2 employee, you’ll typically need to use self-employed loan programs.

Texas has a thriving self-employment economy. Real estate agents, construction contractors, consultants, small business owners, and professionals across industries face the same challenge: their actual income doesn’t match what appears on their tax returns.

The Self-Employed Income Documentation Challenge

Here’s the frustrating reality. You’re running a successful business, depositing healthy amounts into your bank account each month, and managing your finances responsibly. But when you apply for a traditional mortgage, the lender focuses entirely on your tax returns.

And those tax returns? They show minimal income because you’ve strategically used business deductions to reduce your tax burden. Vehicle expenses, home office deductions, equipment purchases, travel costs. All perfectly legal and financially smart. But they make you look broke on paper.

Traditional lenders see your adjusted gross income and say you don’t qualify. Meanwhile, your bank account tells a completely different story. This disconnect is exactly why alternative documentation loans exist.

Bank Statement Loans: The Primary Alternative for Self-Employed Buyers

Bank statement loans have become the go-to solution for self-employed borrowers. They’re the closest thing to the old stated income loan self employed buyer programs, but with actual verification.

What Is a Bank Statement Loan and How Does It Work?

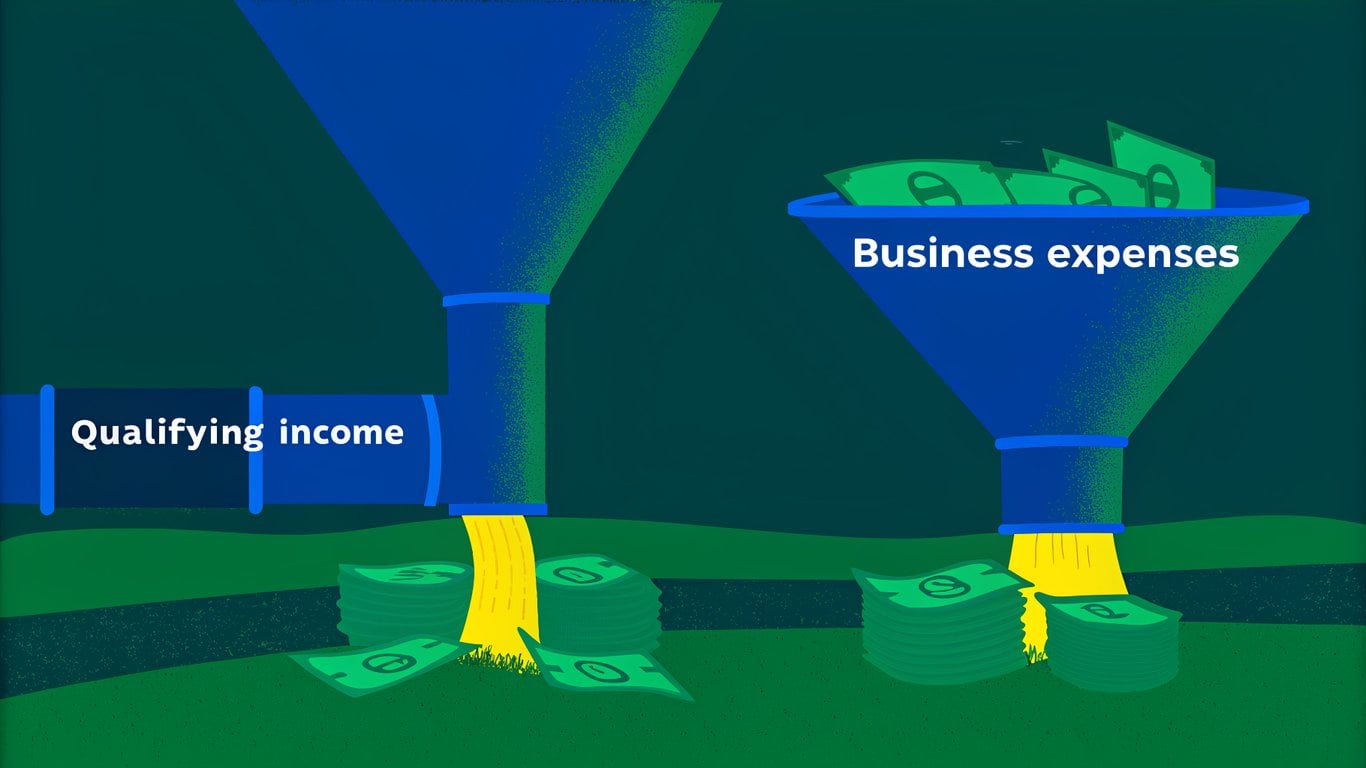

A bank statement loan lets you qualify using your bank deposits instead of tax returns. Lenders review 12 or 24 months of bank statements to calculate your average monthly income. They’re looking at the money actually flowing through your accounts, not what you reported to the IRS.

The process is straightforward. You provide consecutive monthly statements from your business or personal accounts. The lender adds up your deposits, applies an expense ratio, and determines your qualifying income. No tax returns required.

12-Month vs. 24-Month Bank Statement Programs

Most lenders offer both 12-month and 24-month programs. The 12-month option requires only one year of statements but typically comes with stricter requirements. You’ll probably need a higher credit score and larger down payment.

The 24-month program uses two years of statements, which gives lenders more confidence in your income stability. This often results in better terms and lower rates. If your income has been consistent or growing, the 24-month option usually works in your favor.

How Lenders Calculate Income from Bank Statements

Lenders don’t count every dollar that hits your account. They apply an expense ratio to account for business costs. This ratio typically ranges from 25% to 50%, depending on your business type and the lender’s guidelines.

Here’s an example. Say your bank statements show $10,000 in monthly deposits. If the lender applies a 40% expense ratio, they’ll calculate your qualifying income as $6,000 per month. That’s the number they’ll use for your debt-to-income ratio.

Some lenders use different expense ratios for different industries. A consultant might get a 25% ratio since they have minimal overhead. A contractor might see 50% because of material costs and equipment expenses.

Personal vs. Business Bank Statements: What You Can Use

You can use personal bank statements, business bank statements, or a combination of both. Many self-employed borrowers run income through personal accounts, especially sole proprietors and freelancers. That’s perfectly acceptable.

Business accounts work too, obviously. If you have an LLC or corporation with separate business banking, those statements show your income just as well. Some lenders prefer business accounts because they demonstrate more formal business structure.

Mixing both types can work, but it requires careful documentation. You’ll need to show that you’re not double-counting income that flows from business to personal accounts.

Advantages of Bank Statement Loans for Texas Self-Employed Buyers

The biggest advantage is obvious: you don’t need tax returns. Your actual cash flow determines your qualification, not your taxable income. This levels the playing field for self-employed borrowers who use legitimate tax strategies.

Approval often happens faster than traditional mortgages. There’s less documentation to gather and verify. You’re not waiting for tax transcripts from the IRS or dealing with complex business financial statements.

For high-earning self-employed professionals, bank statement loans can actually qualify you for more house than a traditional mortgage would. Your deposits reflect your true earning power.

Stated Income Loan Requirements: What Lenders Look For

Alternative documentation loans aren’t easier to get. They’re just different. Lenders still evaluate your creditworthiness carefully, they just use different metrics.

Credit Score Requirements and Standards

Most bank statement loan programs require a minimum credit score between 620 and 680. Some lenders go as low as 600, but you’ll pay significantly higher rates. The sweet spot for decent terms is usually 680 or above.

Your credit score affects your interest rate more dramatically with these loans than with conventional mortgages. A 640 score might cost you an extra percentage point compared to a 720 score.

Down Payment Expectations for Self-Employed Buyers

Expect to put down at least 10% to 20%. Some programs allow 10% down, but 15% to 20% is more common and gets you better terms. The larger your down payment, the lower your rate and the easier your approval.

Texas doesn’t have specific down payment requirements that differ from other states, but the competitive housing market in cities like Austin, Dallas, and Houston means you’ll want every advantage you can get.

Debt-to-Income Ratios and How They’re Calculated

Lenders typically want to see a debt-to-income ratio of 50% or less, though some programs allow up to 55%. Remember, they’re calculating your income based on bank deposits minus the expense ratio, not your tax returns.

Your DTI includes your proposed mortgage payment plus all other monthly debt obligations. Credit cards, car loans, student loans, and other mortgages all count. Business debts that appear on your personal credit report count too.

Cash Reserves and Asset Requirements

Most lenders require 6 to 12 months of reserves. That means liquid assets equal to 6 to 12 months of your proposed mortgage payment sitting in bank accounts or investment accounts after closing.

Reserves demonstrate financial stability. Self-employed income can fluctuate, and lenders want assurance you can handle a slow month or unexpected business expense without defaulting on your mortgage.

Business Stability and Income Consistency

Lenders typically want to see at least two years of self-employment history. They’re looking for consistent or increasing income over that period. Wild fluctuations raise red flags.

You’ll need to provide documentation proving your business exists and operates legitimately. Business licenses, client contracts, or a CPA letter can help establish your business stability.

Property Type and Loan Amount Limitations

Most bank statement loan programs work for primary residences, second homes, and investment properties. Single-family homes, condos, and townhomes typically qualify. Some lenders have restrictions on rural properties or unique property types.

Loan limits vary by lender but often go up to $3 million or more. Texas doesn’t have conforming loan limits that affect these programs since they’re already non-conforming loans.

Additional Stated Income Loan Alternatives for Texas Self-Employed Buyers

Bank statement loans aren’t your only option. Several other programs serve self-employed borrowers with different financial situations.

Asset-Based Mortgage Loans (Asset Depletion Loans)

If you have substantial assets but irregular income, asset-based loans might work better. Lenders calculate your qualifying income by dividing your liquid assets by 360 months (30 years). If you have $1 million in investment accounts, that’s roughly $2,778 per month in qualifying income.

These loans work well for retirees, investors, or business owners who’ve accumulated significant wealth but show minimal income on tax returns.

Profit and Loss Statement Loans (P&L Loans)

Some lenders accept CPA-prepared profit and loss statements instead of tax returns. Your accountant creates a detailed P&L showing your business income and expenses for the past 12 or 24 months.

P&L loans typically require the CPA to be licensed and have a relationship with your business. They can’t just prepare a one-time statement for your mortgage application.

Debt Service Coverage Ratio (DSCR) Loans for Investment Properties

If you’re buying a rental property, DSCR loans qualify you based on the property’s rental income, not your personal income. The lender calculates whether the rent covers the mortgage payment plus expenses.

Texas has strong rental markets in major metros, making DSCR loans particularly attractive for self-employed real estate investors. You don’t need to prove personal income at all.

Portfolio Loans from Local Texas Banks and Credit Unions

Some local banks and credit unions keep loans in their own portfolio rather than selling them. This gives them flexibility to create custom lending solutions for self-employed borrowers they know and trust.

Portfolio loans work best when you have an existing relationship with the institution. If you’ve banked with a local credit union for years, they might offer terms that national lenders won’t.

Non-QM Loan Programs: Understanding Your Options

All these alternatives fall under the non-QM umbrella. Non-qualified mortgages don’t meet standard Fannie Mae or Freddie Mac guidelines, but they’re legitimate loans from licensed lenders. They’re just underwritten to different standards.

Non-QM doesn’t mean subprime. These are quality loans for borrowers who don’t fit the conventional box. You’ll pay slightly higher rates, but you’re getting financing that wouldn’t otherwise be available.

Documentation Strategies: How to Prepare for a Stated Income Loan Alternative in Texas

Preparation makes the difference between approval and denial. Start organizing your documentation months before you apply.

Organizing Your Bank Statements for Maximum Approval Chances

Request 24 months of statements from your bank, even if you’re applying for a 12-month program. Having extra documentation ready speeds up the process if the lender requests it.

Make sure your statements are consecutive with no gaps. Missing even one month can delay your approval or require additional documentation. Download official statements directly from your bank rather than creating your own spreadsheets.

What to Do About Irregular Deposits and Income Fluctuations

Seasonal businesses and project-based income create natural fluctuations. Lenders understand this. What they don’t like is unexplained large deposits or dramatic income drops without context.

Prepare a brief explanation for any unusual deposits. If you received a large payment from a major project, document it. If you had a slow quarter followed by a strong recovery, explain the business cycle.

Separating Personal and Business Expenses

Clean separation between personal and business finances makes underwriting easier. If you’re mixing personal expenses with business income in the same account, start separating them several months before applying.

Lenders get concerned when they see grocery store purchases and utility bills mixed with business deposits. It makes income calculation more complicated and raises questions about your financial organization.

Preparing Supporting Documentation Beyond Bank Statements

Gather business licenses, client contracts, and proof of business existence. A letter from your CPA confirming your self-employment and business stability can strengthen your application significantly.

If you have major clients or contracts, documentation showing ongoing business relationships helps demonstrate income stability. Invoices and payment records support your bank statement deposits.

Working with a CPA: When Professional Statements Help

A CPA-prepared financial statement adds credibility to your application. Even if you’re using bank statements for qualification, having a CPA letter or P&L statement as supporting documentation can help.

The cost for a CPA letter typically ranges from a few hundred to a thousand dollars, depending on complexity. It’s worth the investment if it strengthens your application or opens up additional loan programs.

Timeline: When to Start Preparing Your Documentation

Start preparing at least three to six months before you plan to apply. This gives you time to clean up your accounts, build reserves, and address any credit issues.

If your bank statements show problematic patterns, you need time to establish better documentation. You can’t fix six months of messy banking overnight.

Finding the Right Lender: Where to Get Stated Income Loan Alternatives in Texas

Not all lenders offer these programs. You need to know where to look and what questions to ask.

Types of Lenders That Offer Bank Statement Loans

Non-QM specialists focus exclusively on alternative documentation loans. They understand self-employed borrowers and have streamlined processes. Mortgage brokers can access multiple non-QM lenders and shop programs for you.

Some credit unions and portfolio lenders offer their own versions of bank statement loans. These institutions keep loans on their books and can be more flexible with underwriting.

Why Traditional Banks Don’t Offer These Programs

Major banks like Wells Fargo, Bank of America, and Chase don’t typically offer bank statement loans. They focus on conventional mortgages that meet Fannie Mae and Freddie Mac guidelines because those loans are easier to sell on the secondary market.

Don’t waste time applying at big banks if you need alternative documentation. They’ll just decline your application or try to force you into a traditional mortgage that doesn’t work for your situation.

Working with Mortgage Brokers vs. Direct Lenders

Mortgage brokers access multiple lenders and can shop your scenario to find the best program and rate. This is particularly valuable for self-employed borrowers since different lenders have different guidelines and pricing.

Direct lenders offer their own programs and might provide faster processing since there’s no middleman. But you’re limited to their specific guidelines and pricing.

Questions to Ask Potential Lenders

- How many bank statement loans do you close per month?

- What’s your minimum credit score requirement?

- What expense ratio do you apply to my industry?

- Can I use personal bank statements, business statements, or both?

- What’s your typical interest rate for my credit profile?

- How much in reserves do you require?

- What’s your average time to close?

Red Flags and Lenders to Avoid

Be wary of lenders who promise approval without reviewing your documentation. Legitimate lenders need to see your bank statements and credit before making commitments.

Watch out for excessive fees or rates that seem too good to be true. Verify that any lender you work with is properly licensed in Texas through the NMLS Consumer Access website.

Costs, Rates, and Terms: What to Expect with Stated Income Loan Alternatives

Alternative documentation loans cost more than conventional mortgages. That’s just reality. But the extra cost might be worth it if it’s your only path to homeownership.

Interest Rates: How Much Higher Than Conventional Loans?

Expect rates roughly 0.5% to 2% higher than conventional mortgages. The exact premium depends on your credit score, down payment, and the specific lender. Stronger financial profiles get better pricing.

Texas doesn’t have unique rate considerations compared to other states, but the competitive lending market means you should shop around. Rate differences between lenders can be significant.

Fees and Closing Costs for Bank Statement Loans

Origination fees typically range from 1% to 3% of the loan amount. Some lenders charge higher underwriting fees for non-QM loans because they require more manual review.

Total closing costs usually run 2% to 5% of the purchase price, similar to conventional loans. The difference is mainly in the origination and underwriting fees.

Loan Terms and Prepayment Penalties

Most bank statement loans come with 30-year terms, though 15-year and other options exist. Some programs include prepayment penalties, typically lasting one to three years. These penalties compensate lenders for the higher risk and cost of originating non-QM loans.

Always ask about prepayment penalties upfront. If you plan to refinance once your tax returns look better, you need to factor in any penalty costs.

The True Cost Analysis: Is It Worth It?

Calculate the total cost difference over your expected holding period. If you’re paying an extra 1% in interest on a $400,000 loan, that’s $4,000 per year or $333 per month. Over five years, that’s $20,000 in additional interest.

But if the alternative is not buying a home at all, or waiting years until your tax returns qualify you for conventional financing, the extra cost might be worthwhile. Texas home values have appreciated significantly in recent years, and waiting could cost you more in lost equity than you’d save in interest.

Texas-Specific Considerations and Success Tips for Self-Employed Buyers

Texas has unique characteristics that affect self-employed homebuyers. Understanding these factors helps you navigate the process more effectively.

Texas Mortgage Regulations and Consumer Protections

Texas has strong homestead protections that limit how much home equity you can borrow against. While this doesn’t directly affect purchase loans, it’s worth understanding the state’s unique lending environment.

The state requires specific disclosures and has regulations around cash-out refinances that don’t exist elsewhere. Make sure any lender you work with understands Texas-specific requirements.

Improving Your Approval Odds: Actionable Steps

- Increase your credit score by paying down credit card balances and disputing any errors

- Build cash reserves to at least 12 months of mortgage payments

- Clean up your bank statements by separating personal and business expenses

- Increase your down payment if possible to reduce lender risk

- Reduce your debt-to-income ratio by paying off smaller debts

- Establish consistent deposit patterns for at least six months before applying

Common Mistakes Self-Employed Buyers Make (and How to Avoid Them)

The biggest mistake is waiting until you’re ready to buy before organizing your finances. You can’t fix 12 months of messy bank statements overnight. Start preparing early.

Another common error is applying with traditional banks first. Multiple credit inquiries hurt your score, and big banks will just decline your application anyway. Start with lenders who actually offer the programs you need.

Don’t assume you can’t qualify just because your tax returns show minimal income. Many self-employed buyers give up without exploring alternative documentation options.

Next Steps: Your Action Plan for Getting Approved

Start by pulling your credit report and addressing any issues. Then organize 24 months of bank statements and calculate your average monthly deposits. This gives you a realistic picture of your qualifying income.

Contact two or three mortgage brokers or non-QM lenders who specialize in self-employed borrowers. Get pre-qualified to understand your buying power and what documentation you’ll need.

Contact two or three mortgage brokers or non-QM lenders who specialize in self-employed borrowers. Get pre-qualified to understand your buying power and what documentation you’ll need. Build your reserves if needed, and work on any credit issues. Once you’re confident in your financial position, start house hunting with a clear understanding of your budget and loan options.

Being self-employed doesn’t have to prevent you from buying a home in Texas. The stated income loan self employed buyer programs of today look different than they did before 2008, but they serve the same purpose. With proper preparation and the right lender, you can qualify for financing that recognizes your true earning power rather than just what appears on your tax returns.