You need to sell your house, but you’re not ready to move out yet. Maybe you’re going through a divorce and need time to find a new place. Or you’re settling an estate and the family needs a few months to sort things out. A sell-and-stay program might be exactly what you need.

What Is a Sell-and-Stay Program?

A sell and stay program, also called a sale-leaseback agreement, lets you sell your home and immediately rent it back from the buyer. You get the cash from the sale right away, but you don’t have to pack up and leave. Instead, you become a tenant in your former home for a set period.

This isn’t the same as a traditional rent-back arrangement where you negotiate a few extra weeks after closing. We’re talking about structured programs where the buyer expects to lease the property back to you for months, sometimes even a year or more.

Who Benefits Most from These Programs?

These programs work best for homeowners facing specific challenges. If you’re going through a divorce, you might need to split the equity but can’t afford two new places immediately. Probate situations often require selling the family home while heirs figure out their next steps.

Homeowners facing foreclosure sometimes use sale-leaseback arrangements to avoid losing everything. You sell before the bank takes the house, access your remaining equity, and buy yourself time to stabilize financially. People relocating for work also benefit when they need to sell quickly but their new housing isn’t ready yet.

The Rise of Sale-Leaseback Options in Texas

Texas has seen growing interest in these programs, partly because the state’s real estate market moves fast. When inventory is tight and buyers are competing, traditional sellers often can’t negotiate extended occupancy periods. Sell-and-stay programs fill that gap.

Some real estate investors specifically target these arrangements. They’re willing to wait for possession because they see long-term value in the property. But this also means homeowners need to be careful about who they’re dealing with.

How Sell-and-Stay Programs Work

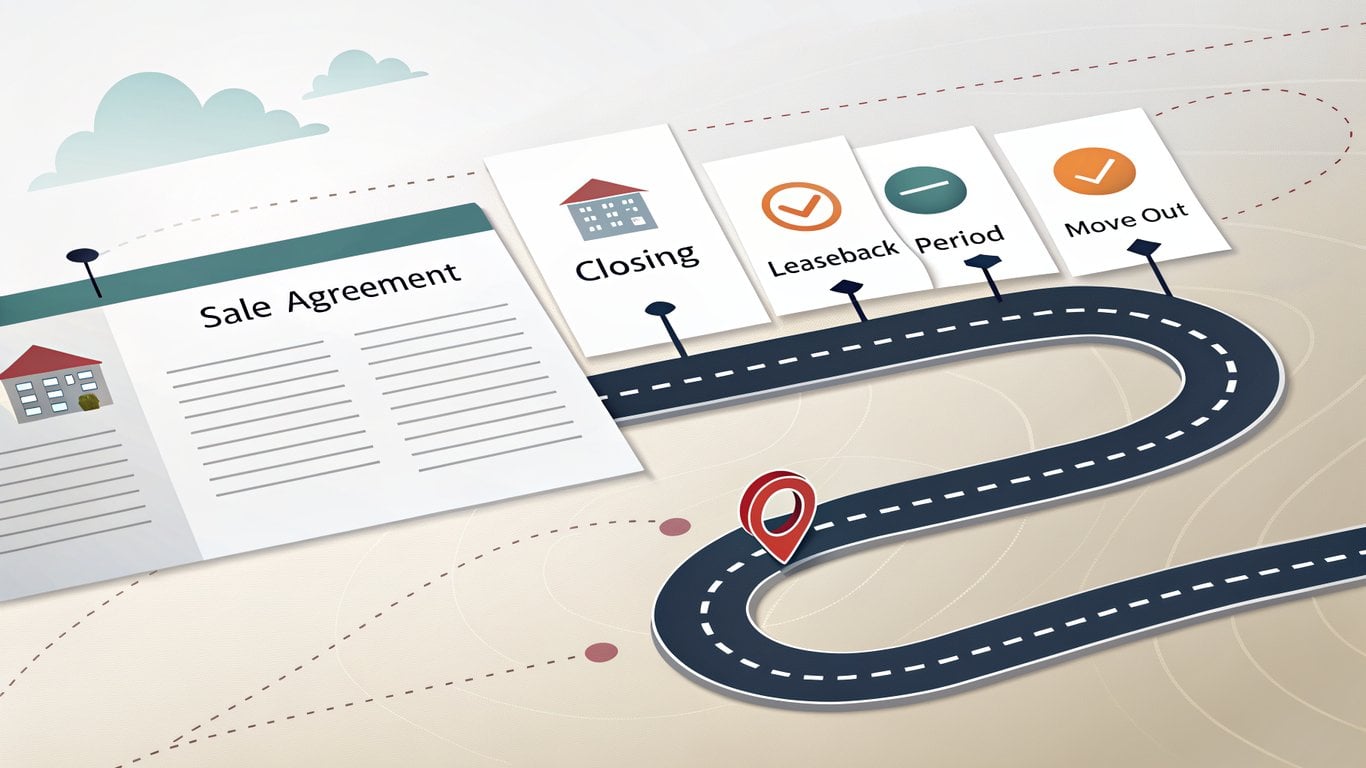

The Initial Sale Transaction

The process starts like any home sale. You agree on a purchase price with the buyer, sign a contract, and go through closing. The difference is that your purchase agreement includes provisions for the leaseback arrangement.

Pricing can be tricky. Some programs offer market value, while others come in below market because they’re providing the convenience of letting you stay. You’ll want to get your home appraised independently to know what fair market value actually is.

The Leaseback Agreement

At closing, you sign two sets of documents. The first transfers ownership of your home. The second is your lease agreement as a tenant. This lease typically starts immediately after closing.

Your rental rate might be set at market rent for similar properties in your area. Or it could be higher or lower depending on the program structure. Some programs charge below-market rent initially but increase it over time to encourage you to move out eventually.

Living in Your Former Home

Daily life doesn’t change much at first. You’re still living in the same house, in the same neighborhood. But you’re now a tenant, which means different responsibilities.

Most lease agreements require you to handle routine maintenance like you did as an owner. You’ll probably still mow the lawn, change air filters, and keep things in good repair. Major repairs like roof replacement or HVAC system failures typically fall to the landlord, but read your specific agreement carefully.

The Exit Strategy

Your lease will have a defined end date. Some programs offer month-to-month arrangements after the initial term, giving you flexibility. Others have firm deadlines.

You’ll need to plan your next move during this period. That’s the whole point of the arrangement. Use the time to find your next home, save for a down payment, or resolve whatever situation led you to this option in the first place.

Timeline: From Listing to Move-Out

A typical sell and stay program might look like this: You contact a buyer or program provider and get an offer within a week. Closing happens in 30-45 days. Your leaseback period could range from three months to a year, depending on what you negotiate.

The entire process from initial contact to final move-out might span anywhere from six months to 18 months. That’s significantly longer than a traditional sale where you’d be out within 30-60 days of closing.

What to Expect in Sale-Leaseback Agreements

Essential Components of the Contract

You’ll actually sign two separate but connected agreements. The purchase agreement covers the sale itself: price, closing date, title transfer, and all the usual home sale terms. The lease agreement covers your tenancy: rent amount, duration, responsibilities, and termination conditions.

These documents should reference each other. The purchase agreement should explicitly state that a leaseback will occur. The lease should reference the sale and confirm that it begins at closing.

Rental Terms and Payment Structure

Rent calculations vary widely. Some programs charge market rate, which you can verify by checking rental listings for similar homes in your area. Others might charge a percentage of the sale price, typically 0.5% to 1% monthly.

You’ll probably pay a security deposit, just like any rental. This might be one or two months’ rent. Payment schedules are usually monthly, due on the first of each month. Some programs deduct rent from your sale proceeds, which sounds convenient but can eat through your equity quickly.

Duration and Renewal Options

Initial lease terms commonly run six to twelve months. Some programs offer shorter three-month terms, while others might go up to two years for specific situations like probate.

Extension options matter. Can you renew if you need more time? What happens if you want to leave early? Good agreements spell this out clearly. Watch for automatic rent increases on renewals, which some programs use to encourage timely departure.

Maintenance and Repair Responsibilities

This is where agreements differ significantly. Some leases make you responsible for everything, treating you almost like you still own the place. Others follow standard landlord-tenant laws where the owner handles major systems and structural issues.

Texas law generally requires landlords to maintain habitable conditions, but your lease might assign more responsibility to you than typical rental agreements. Read this section carefully and understand what you’re agreeing to.

Texas-Specific Legal Considerations

Texas tenant rights apply to you once you’re renting, even though you used to own the home. The new owner must follow proper eviction procedures if you don’t leave when the lease ends. They can’t just change the locks.

Texas doesn’t have specific laws governing sale-leaseback arrangements, so standard real estate and landlord-tenant laws apply. This makes having an attorney review your agreements even more important.

Advantages for Sellers Needing Move Flexibility

Immediate Financial Relief Without Displacement

The biggest advantage is accessing your home equity immediately while keeping a roof over your head. If you’re facing foreclosure or need cash to settle debts, this can be a lifeline.

You get the sale proceeds at closing, minus what you owe on the mortgage and closing costs. That money can resolve financial emergencies, pay off high-interest debt, or fund your next chapter.

Flexibility for Life Transitions

Divorce situations benefit enormously from sell-and-stay programs. You can split the equity without forcing anyone into immediate homelessness. One spouse might stay in the home while finding new housing, or you might alternate if you have kids.

Estate settlements often involve multiple heirs who need time to coordinate. Selling the house resolves the estate, but the leaseback gives everyone breathing room to make thoughtful decisions about what comes next.

Avoiding Foreclosure While Staying Put

If foreclosure is looming, a sell and stay program lets you exit on your terms. You avoid the credit damage of foreclosure, preserve whatever equity remains, and don’t get evicted with nowhere to go.

The rental payments might be more manageable than your mortgage was, giving you time to rebuild financially. Just make sure the rent is actually affordable, or you’re just delaying the inevitable.

Time to Find Your Next Home

House hunting takes time, especially in competitive markets. You can search for the right place without settling for whatever’s available right now. You’re not making desperate decisions because you have to be out by Friday.

This is particularly valuable if you’re buying again. You can save for a down payment, improve your credit, or wait for better market conditions while living in your former home.

Reduced Moving Stress and Costs

Moving once is expensive and stressful. Moving twice because you had to take temporary housing is worse. Sell-and-stay programs eliminate the need for storage units, temporary rentals, or rushing to pack everything in a week.

You can sort through belongings methodically, donate or sell what you don’t need, and move directly to your next permanent home when you’re ready.

Maintaining Community and School Stability

Kids don’t have to change schools mid-year. You can finish out the school year in your current district, then move during summer break. Your daily routines stay intact while you plan your transition.

You keep your same commute, your same neighbors, your same grocery store. Everything stays familiar while you work through whatever challenge brought you to this point.

Warning Signs of Problematic Programs

Below-Market Purchase Offers

Some programs prey on desperate homeowners by offering significantly less than market value. They’ll frame it as a convenience fee for letting you stay, but you shouldn’t accept 20-30% below what your home is worth.

Get an independent appraisal or at least check recent sales of comparable homes in your neighborhood. If the offer seems low, it probably is. A fair program might be 5-10% below market to account for the delayed possession, but not drastically undervalued. For a transparent process, learn how to get a cash offer on your home fast.

Excessive Rental Rates

Watch for rental rates that are way above market. If similar homes in your area rent for $1,500 monthly but your leaseback agreement charges $2,500, that’s a red flag.

High rent eats through your sale proceeds quickly. Some predatory programs use this tactic intentionally, knowing you’ll burn through your equity and end up with nothing when you finally move out.

Unclear or Missing Contract Terms

Legitimate agreements spell everything out clearly. If the contract is vague about rent amounts, lease duration, or what happens if you need to leave early, that’s a problem.

Missing termination clauses, unclear maintenance responsibilities, or ambiguous language about renewals all suggest the buyer is keeping their options open to exploit you later. Professional agreements are detailed and specific.

Pressure Tactics and Rush Decisions

Any buyer who pressures you to sign immediately without time to review or get legal advice is waving a giant red flag. Legitimate programs understand you need time to make such a major decision.

Claims like “this offer expires tomorrow” or “we have other sellers interested” are classic pressure tactics. Walk away. There will be other options if you need them.

Limited or No Legal Review Period

Good programs encourage you to have an attorney review the contracts. They’ll give you time to do this. Programs that discourage legal review or claim it’s unnecessary are hiding something.

You’re selling your home and signing a lease. These are major legal commitments. Anyone who suggests you don’t need a lawyer is not looking out for your interests.

Unrealistic Promises and Guarantees

Be skeptical of promises that you can buy your home back later at the same price. Or guarantees that you can stay as long as you want with no rent increases. These claims are rarely honored.

If something sounds too good to be true, it probably is. Get everything in writing, and have a lawyer verify that the written contract actually delivers what’s being promised verbally.

Lack of Transparency About Buyer Identity

You should know exactly who’s buying your home. If the buyer hides behind complex corporate structures or won’t provide clear information about their company, that’s suspicious.

Research the buyer. Check online reviews, look for complaints with the Better Business Bureau, and verify they’re a legitimate business. Scammers often use shell companies that disappear after taking advantage of sellers.

Alternatives to Sell-and-Stay Programs

Traditional Sale with Extended Closing

You might negotiate a rent-back period with a traditional buyer. Many buyers will let you stay for 30-60 days after closing if you pay daily rent. This works if you just need a little extra time, not months.

The advantage is you’re dealing with a regular home sale, not a specialized program. The disadvantage is most buyers won’t agree to extended periods beyond a couple months.

Home Equity Loans or Lines of Credit

If you need cash but don’t want to sell, a home equity loan or line of credit might work. You borrow against your home’s value and keep ownership.

This only works if you can afford the payments and have enough equity. If you’re already struggling with your mortgage, adding another payment probably isn’t the answer.

Loan Modification or Forbearance

If foreclosure is the issue, contact your lender about modification or forbearance programs. They might reduce your payment, extend your loan term, or pause payments temporarily.

Lenders often prefer working with you over foreclosing. It’s worth exploring before selling, especially if you want to keep your home long-term.

Renting Out Your Home

You could rent your home to someone else and move to cheaper housing yourself. This preserves ownership and might generate income if rent exceeds your mortgage payment.

The downside is becoming a landlord, which comes with responsibilities and risks. And you still need to find somewhere else to live immediately.

Is a Sell-and-Stay Program Right for You?

Questions to Ask Before Committing

Before signing anything, ask these questions: What’s the exact purchase price and how does it compare to market value? What’s the monthly rent and how was it calculated? How long can I stay? What happens if I need to leave early or want to extend? Who handles repairs and maintenance? What are the termination conditions?

Also ask about the buyer’s experience with these programs. How many have they done? Can they provide references from previous sellers? What happens to your security deposit?

Getting Professional Guidance

Hire a real estate attorney to review the contracts before you sign. This isn’t optional. The few hundred dollars you spend on legal review could save you tens of thousands in problems later.

Consider consulting a financial advisor too, especially if you’re using the proceeds to resolve debt or fund retirement. They can help you understand the long-term implications of your decision.

Comparing Multiple Offers

Don’t accept the first offer you get. Contact multiple buyers or programs and compare terms. Look at the total package: purchase price, rent amount, lease duration, and flexibility.

Sometimes a slightly lower purchase price with reasonable rent is better than a higher price with excessive rental rates. Do the math on what you’ll actually net after your rental period ends.

Protecting Yourself Legally

Get everything in writing. Verbal promises mean nothing. Make sure your lease agreement includes clear termination clauses, maintenance responsibilities, and renewal options.

Keep copies of all documents. Document the home’s condition with photos and video at closing. This protects you if there are disputes about damage when you move out.

Next Steps for Texas Homeowners

If you’re considering a sell and stay program, start by getting your home appraised to know its true value. Research multiple buyers and programs. Contact a real estate attorney who handles these transactions.

Take your time. Even if you’re in a difficult situation, rushing into a bad deal will make things worse. The right program can provide breathing room and financial relief. The wrong one can leave you homeless and broke.

These programs aren’t inherently good or bad. They’re tools that work well in specific situations when structured fairly. Your job is making sure you’re getting a fair deal that actually solves your problem rather than creating new ones.